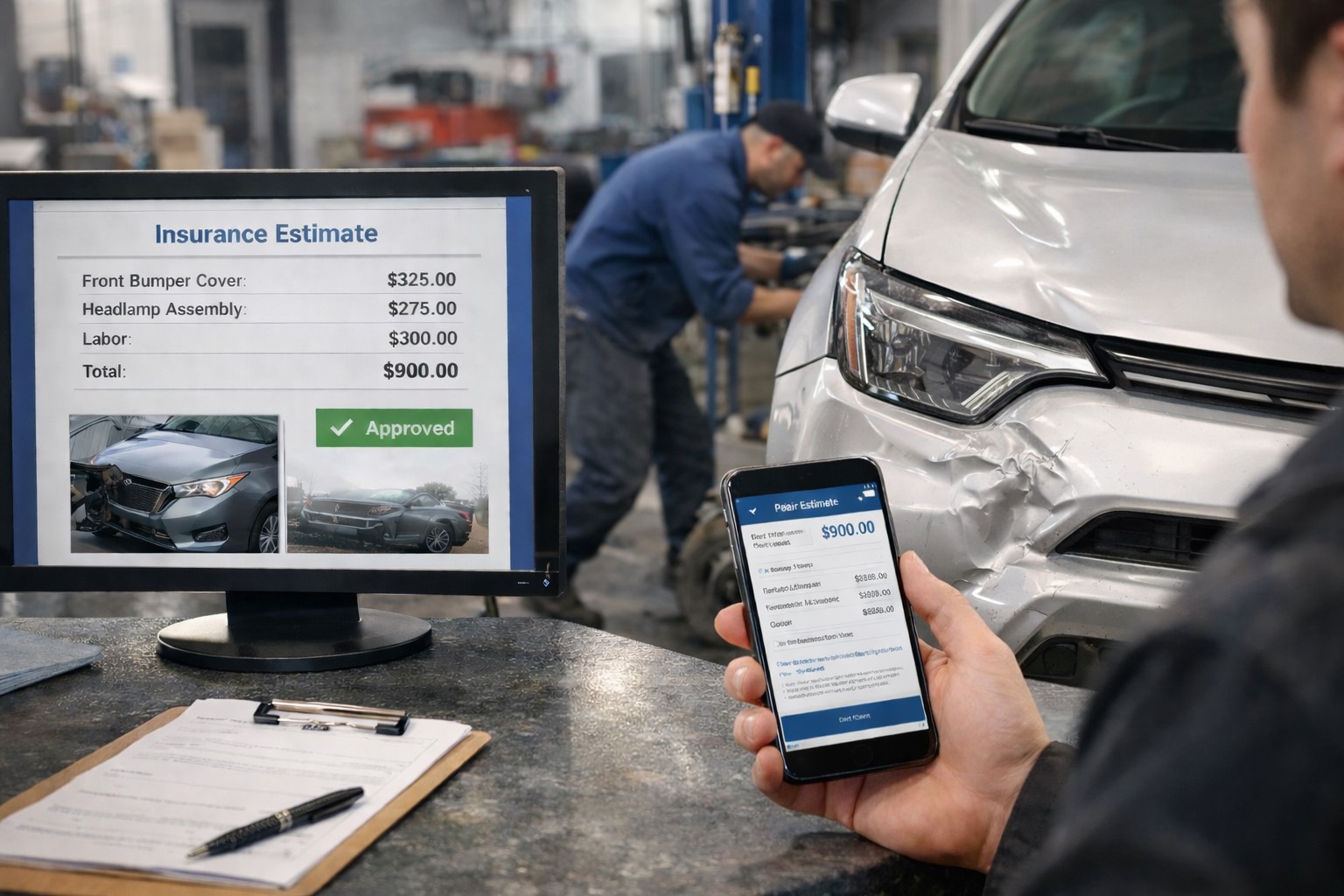

A customer walks in with a clean-looking insurance estimate and assumes the hard part is done. What tends to happen instead is that the first number was built from photos, historical claim data, and software rules that can only price what the camera could see. That matters because the claim now starts with digital confidence, even when the repair still contains unknowns. Major claims platforms already market line-level AI estimating, automated review, and rule-based approval flows for qualified claims.

That system is efficient at the visible layer. It can read exterior damage, match patterns, and move a file forward fast. It cannot fully confirm hidden bracket damage, mounting-point movement, structural displacement, or whether an Advanced Driver Assistance System (ADAS) component disturbance turns into a required calibration once teardown begins. The limitation is not that the software is broken. The limitation is that repair complexity often starts where the photo stops.

The future is not just more photo estimating. The future is broader claims automation around the estimate itself: automated triage, estimate review, file routing, and faster approval paths for losses that fit predefined rules. Claims vendors are openly positioning AI as part of a larger workflow stack, not just a damage-detection tool.

For collision repair shops, that changes the job. The shop is no longer only correcting an incomplete estimate. It is translating physical repair reality into a format that an automated claims system can absorb quickly. Teardown photos, structured documentation, Original Equipment Manufacturer (OEM) procedure support, and well-framed supplements become operational control points.

As insurers accelerate the digital front end of the claim, the shops that stay ahead will be the ones that turn hidden damage into clean, evidence-based supplement files instead of treating every supplement like a fight.